The Taxation System in India is a fundamental mechanism through which governments finance their activities, providing essential public goods and services such as healthcare, education, infrastructure, and national defense. A well-designed taxation system is crucial for economic stability, social equity, and sustainable development. This article of NEXT IAS aims to study in detail the Taxation System in India, its meaning, types of taxation system, types of taxes, and other related concepts.

What is Taxation?

- Taxation refers to the practice of the government collecting money in the form of Taxes from its citizens to finance public services.

- The primary objectives of taxation are to generate revenue for the government to fund public goods and services, ensure economic stability, and promote social equity.

What is Taxation System in India?

- The Taxation System in India refers to the organized structure by which a government collects and manages taxes from individuals and businesses within its jurisdiction.

- Taxation System in India comprises various types of taxes, principles, and mechanisms that determine how much tax is levied, collected, and utilized.

What is Tax?

- Taxes are involuntary fees levied on individuals, businesses, or corporations that are enforced by a government entity, whether local, regional, or national.

- Thus, they are compulsory levies payable by an entity to the government.

- Taxes are the basic source of revenue for the government which is utilized by the government for its various expenses such as Defence, Healthcare, Education, and different infrastructure facilities like roads, dams, highways, etc.

Types of Taxation Method

Various types of taxation method are used under the Taxation System in India and across the world. These taxation methods are described in the sections that follow.

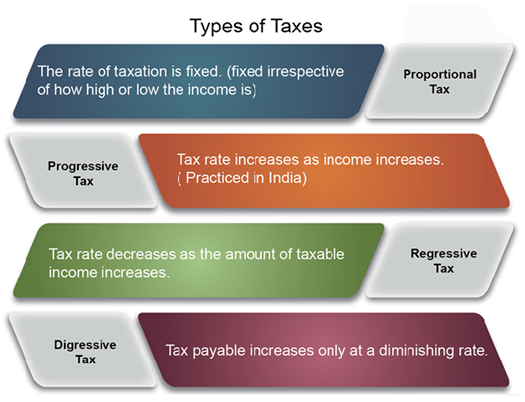

Proportional Taxation or Flat Taxation

- Proportional taxation, also known as Flat Taxation, is a method of taxation system in which the same percentage of income is levied on all taxpayers, regardless of their income level.

- In other words, tax is levied at the same rate for each individual, irrespective of their level of income.

- Here, it is to be noted that the tax rate remains the same, but the absolute amount of tax increases with an increase in income level.

- For example,

| Income Level | Tax Rate | Tax Amount |

| 10,000/- | 10% | 1000/- |

| 1,00,000/- | 10% | 10,000/- |

Progressive Taxation

- Progressive taxation is a method of taxation system in which the tax rate increases as the taxable amount or the income level increases.

- In other words, individuals with higher incomes pay a higher percentage of their income in taxes compared to those with lower incomes.

- Here, the tax rate as well as the absolute amount of tax increases with an increase in income level.

- For example,

| Income Level | Tax Rate | Tax Amount |

| 10,000/- | 10% | 1,000/- |

| 1,00,000/- | 20% | 20,000/- |

Regressive Taxation

- Regressive taxation is a method of taxation system in which the tax rate decreases as the taxable amount or the income level increases.

- In other words, individuals with lower incomes pay a higher percentage of their income in taxes compared to those with higher incomes.

- Here, the tax rate decreases, but the absolute amount of tax increases with an increase in income level.

- However, the increase in the absolute amount of tax w.r.t. increase in income level is lesser than that in the case of proportional and progressive taxation methods.

- For example,

- However, the increase in the absolute amount of tax w.r.t. increase in income level is lesser than that in the case of proportional and progressive taxation methods.

| Income Level | Tax Rate | Tax Amount |

| 10,000/- | 10% | 1,000/- |

| 1,00,000/- | 5% | 5,000/- |

Digressive Taxation

- Digressive taxation is a method of taxation system where the tax rate initially increases with income up to a certain point, after which it either remains constant or decreases.

- Thus, this system of taxation combines elements of both Progressive Taxation and Regressive Taxation.

Methods of Taxation on Goods

There are two methods of levying tax on goods – Ad Valorem and Specific Tax

Ad Valorem

- ‘Ad Valorem’ is a Latin word meaning ‘According to Value’.

- Thus, in the Ad Valorem method of taxation, tax is levied as a percentage of the value of the goods, regardless of the number of units produced.

- For example, 10% on the price of a car.

- In this case, the absolute amount of tax increases with an increase in the price of the car.

Specific Tax

- In the Specific Tax method of taxation, tax is levied as a flat rate per unit of goods produced, regardless of the value.

- For example, 10 lakhs per car.

- Thus, in this case, the tax revenue increases only with the number of units produced, not with the price.

Difference between Ad Valorem and Specific Tax

| Ad Valorem | Specific Tax |

|---|---|

| Based on the assessed value of the product. | Fixed amount tax based on the quantity of units sold. |

| The tax is usually expressed in percentages. Example: GST in India has 5 tax rate slabs- 0%, 5%, 12%, 18% and 28%. | The tax is usually expressed in specific sums. Example: Excise Duty on Petrol. |

| Examples: GST, Property tax, sales tax. | Examples: Excise duty on petrol and liquor products. |

| They are progressive in nature. | They are regressive in nature. |

Impact of Tax

- In the context of Taxation System, the “Impact of Tax” refers to the initial economic burden of the tax i.e. who is directly responsible for paying it to the government.

- For example, in the case of Sales Tax, the seller bears the first responsibility of paying the tax to the government. Thus, in the case of Sales Tax, the seller is the Point of Impact.

Incidence of Tax

- In the context of Taxation System, the “Incidence of Tax” refers to the final economic burden of the tax i.e. who ultimately bears the cost of the tax.

- For example, in the case of Sales Tax, although the seller bears the first responsibility of paying the tax, the tax is ultimately paid by the consumer. So, here, the seller is the Point of Impact and the consumer is the Point of Incidence.

Types of Taxes

Taxes have been, broadly, classified into two types – Direct Taxes and Indirect Taxes.

Direct Tax

- Direct Tax refers to the type of tax that is borne by a person/entity on whom it is levied.

- Thus, in this case, the Impact of Tax and the Incidence of Tax fall on the same person or entity.

- In other words, the burden of a Direct Tax cannot be shifted to another person or entity.

- Direct Taxes in India is administered by the Central Board of Direct Taxes (CBDT), which is a part of the Department of Revenue (under the Ministry of Finance).

- Some prominent examples of Direct Tax include – Income Tax, Corporate Tax, Minimum Alternate Tax, Securities Transaction Tax, etc.

- Various types of Direct Taxes levied and collected in India can be studied in our detailed article on Direct Taxes in India.

Indirect Tax

- Indirect Tax refers to the type of tax for which the Impact of Tax and Incidence of Tax fall on different persons or entities.

- Indirect Taxes are, generally, imposed on goods and services.

- Indirect Taxes in India are administered by the Central Board of Indirect Taxes and Customs (CBIC), which is a part of the Department of Revenue (under the Ministry of Finance).

- Some prominent examples of Indirect Tax include – Customs Duty, GST, etc.

Various types of Indirect Taxes levied and collected in India can be studied in our detailed article on Indirect Taxes in India

Difference between Direct Tax and Indirect Tax

The difference between Direct Tax and Indirect Tax can be seen as follows.

| Basis of Difference | Direct Tax | Indirect Tax |

|---|---|---|

| Liability | Liability (Impact of Tax) as well as the Burden (Incidence of Tax) to pay it resides on the same individual/entity. | Liability (Impact of Tax) to pay the tax lies on a person/entity who then shifts the ultimate Burden (Incidence of Tax) of paying the tax to another individual/entity. |

| Shift in burden | The burden of paying the tax cannot be shifted. | The burden of paying the tax can be shifted. |

| Payment | Paid entirely by a taxpayer directly to the government. | Ultimately paid by the end-consumer of goods and services. |

| Costs of collection | Higher administrative costs of collection. | Lesser administrative costs of collection. |

| Nature | In the case of Direct Taxes, usually, the tax rate increases with increase in income level. So, Direct Taxes are considered progressive in nature. | In the case of Indirect Taxes, the tax rate is the same for all, irrespective of the income level. So, Indirect Taxes are considered regressive in nature. |

| Examples | Income Tax, Corporate Tax, etc. | GST, Entertainment Tax, etc. |

Conclusion

The Taxation System in India is a vital instrument for economic management and social equity. By carefully balancing different types of taxes and adhering to fundamental principles of taxation, governments can create a fair, efficient, and adaptable system that supports public services, promotes economic growth, and ensures the well-being of all citizens. As economies and societies evolve, continuous assessment and reform of Taxaxation System and policies therein are essential to meet new challenges and opportunities.

Tax Base

- In the context of Taxation System, the term “Tax Base” refers to the total value of goods, services, and incomes that are subject to taxation by a government authority.

- Broadening of the Tax Base means that a wider range of goods, services, income, etc., has been made subject to a tax.

Tax Revenue

- In the context of Taxation System, the term “Tax Revenue” is the income that a government collects from taxes imposed on individuals, businesses, and other entities.

- Tax revenue can change through 2 main mechanisms:

- Automatic Changes: These occur without any specific legislative action. For example, Tax Revenue may increase/decrease due to changes in economic activities, inflation, etc.

- Discretionary Changes: These involve changes in Tax Revenue due to deliberate policy decisions by the government. For example, Tax Revenue may increase/decrease due to changes in tax rates, introduction of new taxes, etc.

Adjusted Tax Revenue

In the context of Taxation System, Adjusted Tax Revenue refers to tax revenue calculated after setting aside the change in tax revenue due to discretionary changes.

Tax Buoyancy

- In the context of Taxation System, Tax Buoyancy refers to the responsiveness of tax revenue growth to changes in the Gross Domestic Product (GDP).

- In other words, it measures how much tax revenue increases or decreases when the economy grows or shrinks without any changes in tax rates.

- Tax Buoyancy is measured as follows:

Tax Buoyancy = Proportionate change in tax revenue/proportionate change in GDP

Tax Elasticity

- In the context of Taxation System, Tax Elasticity refers to the responsiveness of tax revenue growth to changes in tax rates.

- In other words, it measures how much tax revenue increases or decreases when the tax rate is increased or decreased, assuming everything else stays the same, like economic activity.

- Tax Elasticity is measured as a proportionate change in tax revenue, without any discretionary change, relative to GDP.

Tax Elasticity = proportionate change in Adjusted Tax Revenue/proportionate change in GDP

- Thus, Tax Buoyancy accounts for the total change in Tax Revenue. However, Tax Elasticity accounts for only an automatic increase in Tax Revenue.

Tax to GDP Ratio

- Tax to GDP Ratio is a measure that compares a country’s total tax revenue to its Gross Domestic Product (GDP).

- It provides an indication of the government’s ability to generate revenue relative to the size of the economy.

- It is expressed as a percentage of the GDP.

Tax to GDP Ratio = (Gross Domestic Product (GDP)/Total Tax Revenue)×100

- A higher Tax to GDP ratio means that the government is able to cast its fiscal net wide, and hence is less dependent on borrowings.

- Thus, the higher the Tax to GDP ratio, the better the health of taxation system, and the better financial position the country will be in.

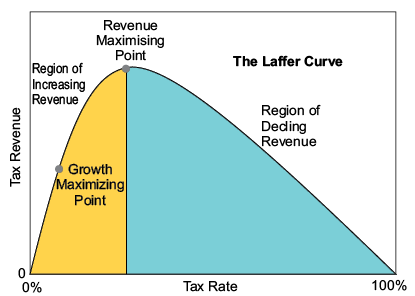

Laffer Curve

- The Laffer Curve was invented by Arthur Laffer.

- It shows the relationship between Tax Rates and Tax Revenue collected by the government.

- The shape of the Laffer Curve is inverted U, which depicts that:

- At a 0% tax rate, the government collects no tax revenue (represented by the leftmost point of the curve at the bottom).

- As the tax rate increases from 0%, government tax revenue initially increases.

- There’s a theoretical sweet spot on the curve where the tax rate generates the maximum amount of tax revenue for the government.

- This point is often referred to as the Optimum Tax Rate.

- Beyond the optimal point, if tax rates continue to rise, government tax revenue starts to decrease.

- This is because high tax rates can discourage economic activity, incentivize tax avoidance, or lead to reduced income levels.

- So, overall, the Laffer Curve says that at a lower as well as higher rate of tax, the tax revenue is low. But, at the optimal rate of tax, the tax revenue is high.

Negative Income Tax (NIT)

- Negative Income Tax (NIT) is a concept in taxation system in India and social policy where individuals earning below a certain income threshold receive supplemental payments from the government instead of paying taxes.

- For example, Subsidy is a Negative Income Tax (NIT).

- The concept of Negative Income Tax (NIT) is aimed to create a more equitable income distribution and provide a safety net for low-income individuals and families.

Pigovian Taxes

- Pigovian Tax, named after the British economist A.C. Pigou, is a tax imposed on activities that generate negative externalities (unintended adverse effects) on third parties or society.

- The primary purpose of a Pigovian Tax is to correct market inefficiencies by internalizing the external costs associated with certain economic activities, thereby aligning private costs with social costs.

- For example, the Carbon Tax is a form of Pigovian Tax, which aims to discourage fossil fuels and encourage renewable sources to tackle climate change threats.

Tobin Tax or Financial Transaction Tax (FTT) or Robin Hood Tax

- Tobin Tax is named after American economist James Tobin.

- Tobin Tax is also known as Financial Transaction Tax (FTT) or Robin Hood Tax.

- It is a proposed tax on currency transactions with an aim to reduce speculative trading in the foreign exchange markets.

- It is to be noted that it proposed taxing only short-term speculative currency transactions.

- Thus, long-term investment, such as FDI, will not suffer from Tobin Tax, as it does not invest for speculative (short-term) reasons like FIIs.

Robot Tax

- Robot Tax is a proposed levy on the use of robots and automation technologies in the workplace.

- The underlying idea is to address the economic and social impacts of increasing automation, particularly the displacement of human workers and the consequent loss of income tax revenue.

- The concept of a robot tax has gained attention as advancements in robotics and artificial intelligence (AI) accelerate, raising concerns about job losses and economic inequality.

Presumptive Tax

- Presumptive taxation is a simplified taxation system designed for small businesses and professionals with a relatively low turnover.

- Unlike the traditional approach where expenses are deducted from revenue to find taxable income, presumptive taxation estimates income based on a pre-determined percentage of total business turnover.

- This eliminates the need for businesses to maintain detailed expense records, simplifying tax filing and reducing administrative costs.

- Only small businesses and professionals, that have a turnover below a set maximum threshold, are eligible under the presumptive taxation scheme.

Tax Deduction at Source (TDS)

- Tax Deduction at Source (TDS) is a mechanism of income tax collection under the Taxation System in India.

- A person (deductor) who is liable to make payment of a specified nature to any other person (deductee) shall deduct tax at source and remit the same into the account of the Central Government.

- For example, an employer deducts TDS from the salary paid to an employee.

- It ensures that the government collects tax as soon as the income is earned, rather than waiting for the end of the financial year.

Tax Shelter

- In the context of Taxation System, Tax Shelter refers to a legal strategy or investment vehicle used by individuals or businesses to reduce their taxable income and overall tax liability.

- These shelters take advantage of provisions in tax laws to minimize the amount of tax owed to the government.

- A tax shelter is entirely different from a tax haven.

- Tax Shelter is a legal way existing within the country to reduce tax liability

- A Tax Haven is a place existing outside the country which provide an illegal way of reducing tax liabilities.

Tax Haven

- In the context of Taxation System, a Tax Haven is a jurisdiction or country that offers favorable tax laws and financial regulations to individuals and businesses, allowing them to minimize their tax liabilities legally.

- Tax havens typically provide low or zero tax rates on certain types of income, as well as strict financial privacy and confidentiality laws.

- These jurisdictions attract individuals and corporations seeking to reduce their tax burdens, protect their assets, and maintain financial privacy.

- Some prominent examples of Tax Haven are – The Cayman Islands, Hong Kong, Mauritius, Panama, Switzerland, etc.

Tax Avoidance

- In the context of Taxation System, Tax Avoidance refers to the legal means by which individuals and businesses structure their financial affairs to minimize their tax liabilities within the bounds of the law.

- There are provisions in the law that allow one to save and invest in a manner that leads to a reduction in taxable income. If these provisions are used for the benefit, it is called Tax Avoidance.

- Unlike Tax Evasion, which involves illegal activities to evade taxes, Tax Avoidance involves exploiting legal loopholes, exemptions, deductions, and other provisions in tax laws to reduce the amount of tax owed.

Tax Evasion

- In the context of Taxation System, Tax Evasion is the illegal act of deliberately underreporting or concealing income, assets, or financial transactions to avoid paying taxes owed to the government.

- Unlike Tax Avoidance, which involves legally minimizing tax liabilities through strategic financial planning and compliance with tax laws, Tax Evasion involves fraudulent and deceptive practices aimed at evading taxes and circumventing tax obligations.

Zero Tax Companies

- In the context of Taxation System in India, Zero Tax Companies are companies that, despite earning significant profits, manage to pay little or no Corporate Tax by making use of various tax deductions, exemptions, credits, and loopholes in the tax system.

- Such companies, although show book profits and may even declare dividends to the shareholders, they do not pay any tax.

- In order to bring such companies under the Income Tax net, Minimum Alternate Tax (MAT) was introduced in 1997-98.

- Now, a company must pay at least either Corporate Tax or Minimum Alternate Tax (MAT), whichever is higher.

| Generally, Income Tax is computed as per the provisions of the Income Tax Act. However, companies compute their book profit as per provisions of the Companies (Amendment) Act, 2019. But, as the Income Tax Act allows several kinds of exemptions, depreciations, and deductions from gross income or book profit, companies are able to show their taxable income as very low. Thus, the amount of tax comes out to be very low. |

Minimum Alternate Tax (MAT)

Minimum Alternate Tax (MAT) refers to the tax imposed on “Zero Tax Companies”, which escape the Corporate Tax net or pay very low taxes by using the provisions of exemptions, deductions, incentives, etc.

Alternate Minimum Tax (AMT)

Alternate Minimum Tax (AMT) is the same as Minimum Alternate Tax (MAT) but is imposed on commercial establishments other than companies, like partnership firms, etc.

Global Minimum Tax (GMT)

- Global Minimum Tax (GMT) is a proposed international tax policy that aims to establish a floor on corporate tax rates worldwide, ensuring that multinational corporations (MNCs) pay a minimum level of tax regardless of where they operate or where their profits are booked.

- The concept of a global minimum tax has gained traction in taxation system in the recent years as countries seek to address tax avoidance, profit shifting, and erosion of their tax bases due to aggressive tax planning by multinational corporations.

Advance Ruling

- In the context of taxation system, an Advance Ruling is a written interpretation of tax laws.

- It is issued by tax authorities to corporations and individuals who request for clarification on certain tax matters.

- It helps in clarifying tax-related rules and showing a clear picture of future tax liability. This, in turn, helps in attracting more Foreign Direct Investment (FDI) as well as reducing tax litigations.

Cess

- Cess is a form of tax levied by the government on top of an existing tax.

- Thus, it is a tax on tax.

- It’s typically imposed for specific purposes and often earmarked for those purposes.

- For example, Education Cess, Swachh Bharat Cess, etc.

Surcharge

- Similar to Cess, a Surcharge is an additional fee or tax added on top of an existing charge.

- It differs from a Cess in that while a Cess is levied and used for a specific purpose, a Surcharge can be used for multiple purposes.

FAQs on Taxation System in India

Which Taxation System is followed in India?

Taxation System in India can be called a multi-layered taxation system which includes both direct and indirect taxes, administered at both the central and state levels.

Who introduced the tax system in India?

Taxation System in India has a long history and has evolved over the centuries. But, the modern taxation system in India, as we know today, was introduced in 1860 by Sir James Wilson, the first Finance Minister in British India.